Bank, can you lend me the rest of the quantity I require for that home, which is essentially $375,000 (how to reverse mortgages work). I'm putting 25 percent down, this right, this right, this number right here, that is 25 percent of $500,000. So, I ask the bank, can I have a loan for the balance? Can I have a $375,000 loan? And the bank says, sure, you look like, uh, uh, a great guy with a great job who has an excellent credit rating.

We have to have that title of the home and as soon as you settle the loan we're going to provide you the title of the house. So what's going to occur here is we're going to have the loan is going to go to me, so it's $375,000, $375,000 loan - how do reverse mortgages work?.

But the title of the home, the file that states who in fact owns your home, so this is the house title, this is the title of the house, house, home title. It will not go to me. It will go to the bank, the house title will go from the seller, perhaps even the seller's bank, perhaps they have not paid off their home mortgage, it will go to the bank that I'm obtaining from.

So, this is the security right here. That is technically what a mortgage is. This vowing of the title for, as the, as the security for the loan, that's what a home loan is. And in fact it originates from old French, mort, means dead, dead, and the gage, suggests pledge, I'm, I'm a hundred percent sure I'm mispronouncing it, but it comes from dead promise.

When I pay off the loan this pledge of the title to the bank will pass away, it'll come back to me. Which's why it's called a dead promise or a mortgage. And probably due to the fact that it originates from old French is the factor why we do not say mort gage. We state, home loan.

The Definitive Guide to How Do Business Mortgages Work

They're actually describing the home loan, home mortgage, the mortgage loan. And what I wish to carry out in the rest of this video is utilize a little screenshot from a spreadsheet I made to really show you the math or really reveal you what your home mortgage payment is going to. And you can download, you can download this spreadsheet at Khan Academy, khanacademy.org/downloads, downloads, slash home loan calculator, home mortgage, or really, even much better, just go to the download, just go to the downloads, downloads, uh, folder on your web browser, you'll see a bunch of files and it'll be the file called home mortgage calculator, home loan calculator, calculator dot XLSX.

But simply go to this URL and then you'll see all of the files there and then you can just download this file if you want to play with it. how do fixed rate mortgages work. However what it does here remains in this type of dark brown color, these are the assumptions that you might input which you can change these cells in your spreadsheet without breaking the entire spreadsheet.

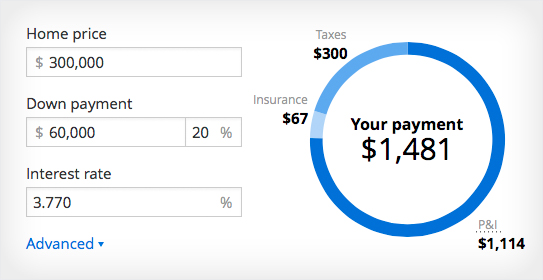

I'm purchasing a $500,000 home. It's a 25 percent down payment, so that's the $125,000 that I had conserved up, that I 'd spoken about right over there. And then the, uh, loan amount, well, I have the $125,000, I'm going to need to borrow $375,000. It determines it for us and then I'm going to get a pretty plain vanilla loan.

So, thirty years, it's going to be a 30-year fixed rate home loan, fixed rate, repaired rate, which indicates the rate of interest won't alter. We'll talk about that in a bit. This 5.5 percent that I am paying on my, on the money that I obtained will not change over the course of the 30 years.

Now, this little tax rate that I have here, this is to actually figure out, what is the tax cost savings of the interest reduction on my loan? And we'll talk about that in a second, we can overlook it for now. how do reverse mortgages work?. And then these Discover more here other things that aren't in brown, you shouldn't tinker these if you really do open this spreadsheet yourself.

Examine This Report about How Do Lendsure Mortgages Work

So, it's literally the yearly rates of interest, 5.5 percent, divided by 12 and a lot of home loan are intensified on a regular monthly basis. So, at the end of on a monthly basis they see how much money you owe and after that they will charge you this much interest on that for the month.

It's really a pretty intriguing problem. But for a $500,000 loan, well, a $500,000 house, a $375,000 loan over 30 years at a 5.5 percent rates of interest. My home loan payment is going to be approximately $2,100. Now, right when I bought the house I wish to present a bit of vocabulary and we've talked about this in a few of the other videos.

And we're presuming that it deserves $500,000. We are presuming that it's worth $500,000. That is an asset. It's an asset https://www.liveinternet.ru/users/galimeh8du/post474134341/ since it offers you future advantage, the future advantage of being able to reside in it. Now, there's a liability against that asset, that's the home loan, that's the $375,000 liability, $375,000 loan or debt.

If this was all of your possessions and this is all of your financial obligation and if you were basically to offer the possessions and pay off the financial obligation. If you sell your home you 'd get the title, you can get the cash and then you pay it back to the bank.

However if you were to relax this transaction right away after doing it then you would have, you would have a $500,000 house, you 'd settle your $375,000 in financial obligation and you would get in your pocket $125,000, which is exactly what your original down payment was however this is your equity.

All About How Mortgages Payments Work

However you could not presume it's consistent and play with the spreadsheet a little bit. However I, what I would, I'm introducing this because as we pay for the debt this number is going to get smaller sized. So, this number is getting smaller, let's state eventually this is just $300,000, then my equity is going to get bigger.

Now, what I've done here is, well, in fact before I get to the chart, let me really reveal you how I compute the chart and I do this over the course of 30 years and it goes by month. So, so you can think of that there's in fact 360 rows here on the real spreadsheet and you'll see that if you go and open it up.

So, on month no, which I don't show here, you borrowed $375,000. Now, over the course of that month they're going to charge you 0.46 percent interest, keep in mind that was 5.5 percent divided by 12. 0.46 percent interest on $375,000 is $1,718.75. So, I haven't made any mortgage payments yet.

So, now prior to I pay any of my payments, instead of owing $375,000 at the end of the first month I owe $376,718. Now, I'm a hero, I'm not going to default on my mortgage so I make that very first mortgage payment that we determined, that we calculated right over here (how do home mortgages work).